7:52

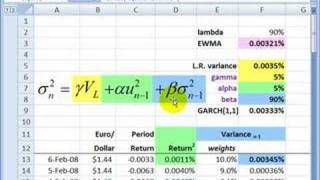

FRM: GARCH(1,1) to estimate volatility

Bionic Turtle

8:24

FRM: Forecast volatility with GARCH(1,1)

10:32

Know the Basics of ARCH Modeling (Part 1)#arch #volatility #modeling #econometrics #financialmodels

CrunchEconometrix

7:17

Know the Basics of ARCH Modeling (Part 2) #arch #volatility #modeling #econometrics #financialmodel

7:09

(EViews10) - How to Estimate ARCH Models #arch #timeseries #volatility #modeling #econometrics

14:45

Volatility: GARCH 1,1 (FRM T2-23)

4:33

Financial models with long-tailed distributions and volatility clustering

WikiAudio

7:45

Что такое Стационарные и нестационарные временные ряды?

Основы анализа данных

1:27:26

Лекция 10 Прогнозирование временных рядов

Data Mining in Action

1:10:01

008. Прогнозирование временных рядов - К.В. Воронцов

Yandex for ML

32:37

Time series met AutoML (Codalab Automated Time Series Regression) — Denis Vorotyntsev

Data Challenges

42:22

Pranav Bahl, Jonathan Stacks - Robust Automated Forecasting in Python and R

PyData

5:16

Модель авторегрессии и скользящего среднего ARMA(p,q)

17:03

How to identify ARIMA p d and q parameters and fit the model in Python

Data Science Tutorials

13:30

Autocorrelation Function (ACF) vs. Partial Autocorrelation Function (PACF) in Time Series Analysis

Data View Analytics

8:56

FRM: Exponentially weighted moving average (EWMA)

8:58

An Introduction to ARCH Models

Morten Nyboe Tabor

12:56

How to Find The Best Time to Trade: Implied Volatility, Explained | Options for Beginners

tastylive

27:48

Historical vs. Implied Options Volatility - Options Mechanics

Option Alpha

13:25

VIX Index Explained | Options Trading Guide

projectfinance

6:09

5 Global Data Sources Every Data Scientist Should Know About! Build Great Machine Learning Models

AI Tourist - Tech Meanderings

7:38

Vector Auto Regression : Time Series Talk

ritvikmath

13:53

Unit Roots : Time Series Talk

10:25

GARCH Model : Time Series Talk

21:23

Integration, Cointegration, and Stationarity

Quantopian

6:11

Cointegration - an introduction

Ben Lambert

27:42

Векторная авторегрессия (практика)

Айрат Галямов

19:30

Cointegration

Jochumzen

4:10

Python Tutorial: Intro to AR, MA and ARMA models

DataCamp

8:04

Fun with Seasonal Adjustment

jodiecongirl

11:43

Python for Financial Analysis and Algorithmic Trading : ARIMA with Statsmodels

WEBHELP 4U

1:28:35

Коинтегрированный арбитраж

Робот Крафт

12:31

Математические методы прогнозирования объемов продаж — Константин Воронцов

ПостНаука

11:22

The error correction model

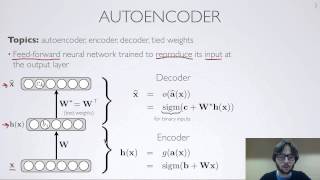

6:15

Neural networks [6.1] : Autoencoder - definition

Hugo Larochelle

29:40

Time Series Anomaly Detection with LSTM Autoencoders using Keras & TensorFlow 2 in Python

Venelin Valkov

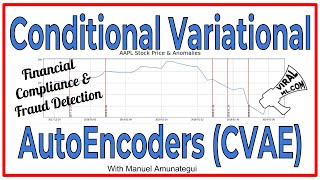

13:23

Learn Financial Compliance & Fraud Detection with Conditional Variational AutoEncoders (CVAE)

42:54

Lecture 13 Time Series Analysis

Jordan Kern

20:37

Fortune-Telling with Python: An Intro to Facebook Prophet

Chicago Python Users Group

20:24

Forecasting at Scale: How and Why We Developed Prophet for Forecasting at Facebook

Lander Analytics

3:57

Парадокс Симпсона [minutephysics на русском]

Eye of modernity

19:15

Forecasting Demand, Finding Sales Data - Facebook Prophet, Google Trends & Python

10:29

Time Series Talk : ARCH Model

8:05

Why Are Time Series Special? : Time Series Talk

3:28

Automatic ARIMA Forecasting

EViews

7:16

Происхождение марковских цепей

edyo.ru

1:08:22

Data Science - Part XIII - Hidden Markov Models

Derek Kane

11:02

7 2 Скрытые марковские модели Hidden Markov Models

Ирина Кузьмина

6:53

Cointegration Test in python

QuantAlpha

6:32

Cleaning Time Series Data : Time Series Talk

7:12

Time Series Talk : ARMA Model

ECONOMETRICS | Autoregressive Distributed Lag Model

Andrei Galanchuk

4:39

Volatility Trading: The Market Tactic That’s Driving Stocks Haywire | WSJ

The Wall Street Journal

12:22

Johansen Cointegration Test. Model One. EVIEWS

Sayed Hossain

5:49

Как определить автокорреляцию в остатках Дарбин Уотсон

MadKorg TV

6:29

Cointegration tests

9:26

(EViews10):Estimate Johansen Cointegration Test #var #vecm #Johansen #cointegration

13:24

Interpreting the Summary table from OLS Statsmodels | Linear Regression

Bhavesh Bhatt

4:54

Eviews 7: Interpreting the coefficients (parameters) of a multiple linear regression model

Phil Chan (philchan)

10:02

Error correction model - part 1

14:54

Собственные значения и собственные векторы матрицы (4)

ivatrishi

14:25

(EViews10): How to Estimate Standard GARCH Models #garch #arch #volatility #clustering #archlm

(EViews10) - How to Test for ARCH Effects #archeffects #archmodeling #volatility #heteroscedasticity

9:33

(EViews10): Estimate and Interpret VECM (2) #var #vecm #causality #lags #Johansen #innovations

4:48

NumXL: ARCH Test in Excel

NumXL

LIVE

[Deleted video]

9:37

(EViews10) - How to Forecast ARCH Volatility #arch #forecasting #volatility #econometrics #modeling

5:05

HOW TO REMOVE SERIAL CORRELATION? Eviews Part 1

Fawad Paul

1:46

Markov Switching in EViews

[Private video]

Integrating Python with EViews 11

9:35

FRM: Volatility approaches

9:27

Video 10 Estimating and interpreting a GARCH (1,1) model on Eviews

Imperium Learning

10:08

Coding the GARCH Model : Time Series Talk

8:34

FRM: Extreme Value Theory (EVT) - Intro

10:24

Markov Chains : Data Science Basics

27:16

Panel Data. Fixed effect and Random effect. Model Two. EVIEWS

8:09

Fixed and random effects with Tom Reader

University of Nottingham

14:44

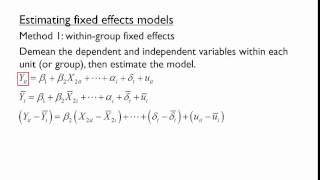

Fixed effects in panel data

Nathan Wozny

28:21

Panel Data Models with Individual and Time Fixed Effects

BurkeyAcademy

40:36

Panel Data Models

econometricsacademy

4:15

Seemingly Unrelated Regressions Example

4:05

Individual Fixed Effects and Time Varying Treatments: Causal Inference Bootcamp

Mod•U: Powerful Concepts in Social Science

2:31

Time Series Bootstrap - Statistical Inference

Data Talks

6:50

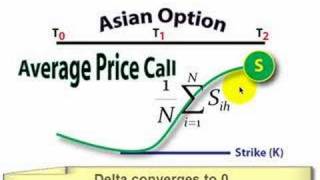

Asian option

1:21:16

9. Volatility Modeling

MIT OpenCourseWare

4:30

Granger Causality in Python : Data Science Code

50:17

Econometrics for Finance - S6 - Volatility Models

UG BSU Elearning and PBL

7:46

FI_V7: Fama-MacBeth Approach for Estimating Market Prices of RIsk

C-RAM

1:10:46

Class 3: Artificial Intelligence in Finance

6:05

ARIMAX | Time Series Model

Analytics Uni - By Biswajit Pani

19:27

Fama French Regression in Python

Algovibes

7:29

2.3 Cross-Sectional Regressions

UChicago Online

9:05

(EViews10):Estimate Chow Test for Structural Break #chowtest #breakpoint #structuralbreak

8:21

STATISTICS I Time Series I Chow Break Test I Intuition and Example

1:37:48

Кирилл Ильинский. Фин. модели: Зачем они нужны и как с ними бороться

Европейский университет в Санкт-Петербурге

12:01

CrunchEconometrix-Teachable P.E.R.B.A. Launch

12:04

Процесс скользящего среднего, MA(q)

2:09:13

Новости нейронауки #4: мозг и алкоголь, формирование памяти, старение / Вячеслав Дубынин в ПостНауке

21:56

58 The #Difference Between #VAR System and #ARDL #Models with Himmy Khan

RESEARCH MADE EASY WITH HIMMY KHAN

15:49

Random Walk in Time Series Analysis | Forecasting | Statistical Analytics

2:44:59

Structural VAR

Econometrics & Dynare

6:25

What is Value at Risk? VaR and Risk Management

Patrick Boyle

58:44

Panel Data Analysis | Econometrics | Fixed effect|Random effect | Time Series | Data Science

11:16

Data Science Interview Question: Stock Price Prediction and Random Walk Hypothesis (Episode 5)

Lazy Programmer

1:32

IMF asks Larry Christiano, what are DSGE models?

IMF

10:35

This video shows how to solve a simple DSGE model

Constantin Bürgi

13:15

1 1 Welcome to Introduction to Computational Finance and Financial Econometrics 1314

Piperude

5:36

Future - Life Is Good (Official Music Video) ft. Drake

Future

12:49

An intuitive introduction to Difference-in-Differences

Doug McKee

45:02

Векторная авторегрессия VAR, коинтеграция временных рядов

1:17:19

Анализ временных рядов

1:21:36

Анализ временных рядов в Python (практика)

1:38:04

Технический анализ. Волатильность. ARCH-модели

(EViews10): How to Estimate Exponential GARCH Models #garchm #tgarch #egarch #igarch #cgarch #arch

9:54

Урок 2, часть 3. Eviews - анализ временных рядов.

СМЫСЛ. Помощь в учёбе

13:04

Урок 2. Часть 1. Eviews. Анализ временных рядов.

9:15

Урок 2, часть 2. Eviews - анализ временных рядов.

17:44

Removal of Heteroscedasticity. Model One. EVIEWS

8:22

Eviews- how to detect and remove heteroskedasticity

Econ Academy

24:37

ARCH-M Model. Model One. Part 1 of 3. EVIEWS

9:57

An Introduction to GARCH Models

25:25

ARCH-M Model. Model One. Part 2 of 3. EVIEWS

18:00

ARCH-M Model. Model One. Part 3 of 3. EVIEWS

0:55

Бассейн

denisbaranoff

2:35

GARCH-in-mean model - Eviews

EssentialsofTimeSeries_Book

(EViews10): How to Estimate GARCH-in-Mean Models #garchmodels #garchm #tgarch #volatility #egarch

10:07

(EViews10): Heteroskedasticity and Weighted (Generalised) Least Squares #gls #wls #ols #weights

9:59

Understanding Heteroskedasticity #errorvariances #gls #wls #ols #homoscedasticity

15:53

(EViews10): How to Detect Heteroskedasticity #errorvariances #graphs #plots #variances #archlm

17:16

An Introduction to Multivariate GARCH

Rasmus Pedersen

17:46

GARCH in mean (GARCH-M) model: volatility persistence and risk premia (Excel)

NEDL

33:21

Algorithmic trading in Python: Cointegration and pair trading

4:20

Bebe Winans, Brian McKnight ft. Joe - Coming Back Home (Official Video)

Bebe Winans

48:47

Парный линейный регрессионный анализ

Учебные фильмы

26:38

13.2 Разложение функции в ряд Фурье. Пример 1.

N Eliseeva

1:14:02

Онлайн-лекция «Модели и данные: мнения финансовой индустрии и статистические тесты»

Российская экономическая школа

3:21:39

Темный Рыцарь - Корреляция | Кирилл Ильинский | Лекториум

Лекториум

43:29

Cointegration Analysis with Econometrics Toolbox

MATLAB

9:46

Введение в опционы (опцион call и опцион put) | Финансы

KhanAcademyRussian

1:40:13

10. Временные ряды. Курс «Введение в анализ данных» | Технострим

VK Team

24:12

Genesis of GARCH - Why you have been measuring volatility wrong all your life

Dirty Quant

33:54

Measuring and Monitoring Volatility (FRM Part 1 2025 – Book 4 – Chapter 3)

AnalystPrep

7:36

Time Series Talk : White Noise

10:36

Плотность распределения вероятностей

7:50

(EViews10): VAR and Impulse Response Functions (2) #var #irf #impulseresponse #innovations #shocks

53:17

The Bayesians are Coming to Time Series

AICamp

Paul Wilmott on Quantitative Finance, Chapter 3, First Stochastic Differential Equation

Nathan Whitehead

12:44

1.5 Solving Stochastic Differential Equations

20:32

Time series inference with nonlinear dynamics and filtering for control.

Microsoft Research

22:41

Unit Root, Stochastic Trend, Random Walk, Dicky-Fuller test in Time Series

2:13:11

Заниятие 6. 2021-10-15. Интеграл Ито

Mike Andreev